How Much Cash Should Be in Your Portfolio?

If I told you your portfolio grew from $40 million to $140 million over the past decade, you might immediately feel a sense of satisfaction. After all, that’s remarkable growth by any measure. But what if I told you that if you had simply used an ETF on a broad market index, like the S&P 500, you would have earned an extra $30 million more during the same period? Suddenly, the impressive gain doesn’t feel quite as satisfying. This naturally raises the question: Why? The answer may lie in your asset allocation including your cash allocation, your sector allocation, and the fees you’re paying. So, How Much Cash Should Be in Your Portfolio?

Evaluation of investment performance should not be done by growth alone but by relative measurements. By taking into account a consideration of factors such as cash reserves, asset allocation, and fees compared to alternative investment options. In this article, we’ll explore why relying solely on high-level growth numbers can be misleading and how assessing your performance across multiple dimensions can bring clarity and better performance.

The Role of Cash: A Cushion or a Drag?

One of the first elements to consider when evaluating your portfolio’s performance is how much cash you’re holding. Cash can be seen both as a safety net. But, also acts as a growth inhibitor. Since, over the long-run, the rate of return on cash tends to be much lower compared to productive assets such as stocks. Especially after taxes are considered.

Many investors hold onto large cash reserves in their portfolios as a buffer against volatility. Usually, the reasons are psychological rather than empirical. After all, having liquid assets at the ready can be reassuring during market downturns. However, cash in your portfolio also acts as an anchor weighing down your overall growth. When interest rates are low, the returns on cash are negligible, and in an inflationary environment, your cash is effectively losing value over time.

Let’s say you held 20% of your portfolio in cash while the rest was invested in a mix of stocks, bonds, and real estate. That’s 20% of your capital that’s not actively growing in value. While this might feel safe. Over the long term, it will substantially reduce your portfolio’s growth potential.

To evaluate how much your cash holdings have helped or hindered your performance, consider comparing your portfolio’s growth to a simple index, like the S&P 500. If your portfolio grew from $40 million to $140 million, but $170 million would have been achievable, that 20% cash allocation could represent significant missed opportunity.

Asset Allocation: Finding the Right Balance

While cash plays a role in portfolio performance, asset allocation is arguably one of the most significant factors in determining long-term outcomes. Asset allocation refers to how you distribute your investments across different categories like stocks, bonds, real estate, and alternative assets.

Why is asset allocation so important? Different assets have different risk-return profiles. A well-balanced asset allocation should reflect your financial goals, risk tolerance, and investment horizon. However, many investors fall into the trap of either being too conservative or too aggressive in their allocations.

Let’s return to our hypothetical $140 million portfolio. If the portfolio had an overly conservative allocation—perhaps leaning heavily toward bonds and cash—it’s no surprise the growth lagged behind a 100% equity benchmark like the S&P 500. On the other hand, if the allocation was too weighted toward risky equities, the portfolio might have faced sharper draw-downs during market corrections. This could lead to sleepless nights and possibly panicked selling at the wrong time. So, it’s essential to evaluate your portfolio based on how your asset allocation aligns with your long-term goals, not just on headline performance. This approach helps you understand whether you’re truly on the right path.

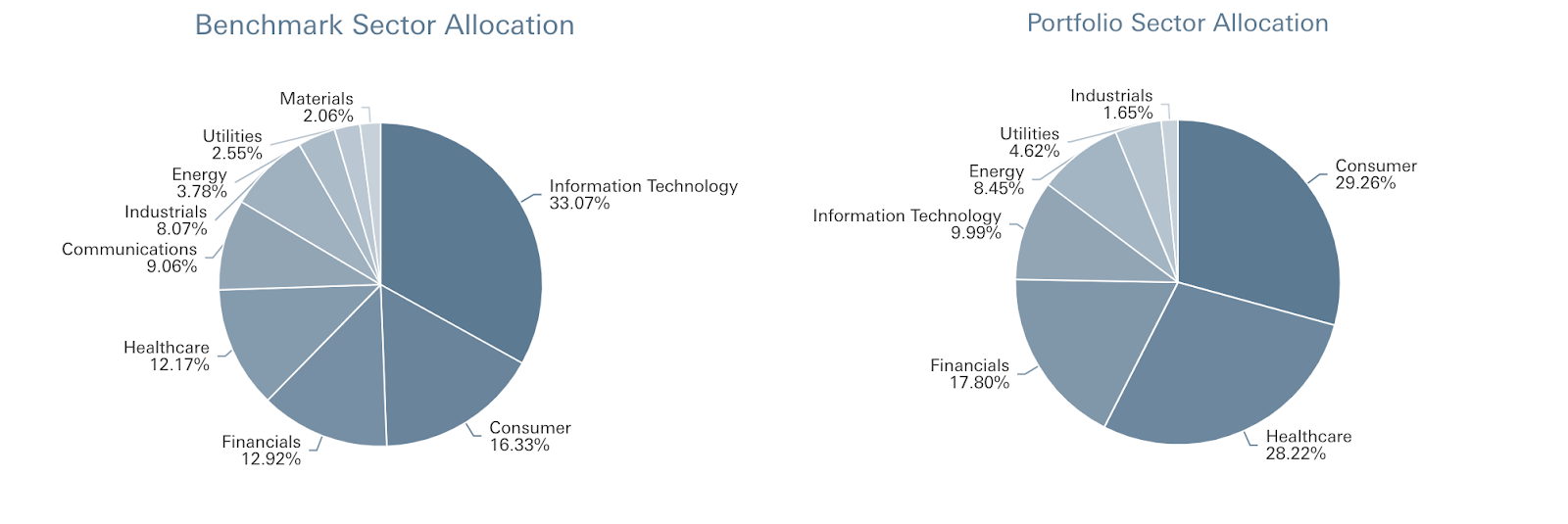

Additionally, sector composition plays a vital role in performance. For instance, the S&P 500’s sector weighting changes over time—technology, healthcare, and financial services have significant influence today. But, if your portfolio is underweight or overweight in certain sectors, you may not be keeping pace with broader market trends. Our family office can show this discrepancy with actual numbers in reports we provide. We can draw direct comparisons between the sector composition of the S&P 500 to your own portfolio. And, by not adjusting for sector exposure, you run the risk of missing out on key growth areas. See here, we can compare your sector breakdown to the benchmark, highlighting areas where your portfolio might be out of sync with market trends.

Fees: The Silent Killer of Returns

Fees are another important factor to consider when evaluating your financial performance. While fees might seem small, they compound over time and can take a significant bite out of your portfolio’s growth.

For example, if you’re paying 1% annually on a $140 million portfolio, that’s $1.4 million each year going toward management costs. Over a decade, this adds up to $14 million. This is not even accounting for the lost investment growth you could have otherwise enjoyed by compounding. Even a seemingly modest reduction in fees can lead to significant savings. Imagine if you could reduce your fees to just 0.05%—the savings over time could be a game-changer.

As a personal CFO, we help our clients organize and focus their financial lives. Our role is to reduce the administrative burden, increase efficiency, and ultimately provide peace of mind. By handling the complexities of your finances and offering clear, organized reporting, we enable you to take a step back from the daily grind of portfolio management and focus on the bigger picture. Our fee is 0.05% for our bookkeeping and reporting service. And, 0.10% for our personal CFO family office service. Our fees are often 10 to 20 times lower than investment management fees. And, we will help show you how to reduce those fees by simplifying your financial life. And, doing a better job of evaluating performance.

How Much Cash Should be in Your Portfolio?

While traditional investment managers often focus on short-term market moves and high-level performance metrics, our approach offers a more sophisticated perspective. Instead of managing individual investments, we take on the role of personal CFO—helping you organize and streamline your financial life. We assist you in focusing on long-term strategies, rather than constantly reacting to market fluctuations.

Our philosophy is that simplicity often yields the best results. By minimizing unnecessary complexity, such as frequent trading or high management fees, you can achieve more consistent results. This approach reduces stress and focuses on long-term growth. We handle the administrative tasks and provide detailed performance reporting. This frees up your time to concentrate on your personal and professional goals. In turn, we help investors realize they don’t need such a large cash allocation since their investments will be paying dividends and interest regularly anyway.

Yes, growing your portfolio from $40 million to $140 million is an achievement. But when you dig deeper and analyze how much cash you’re holding, how your assets are allocated, and how much you’re paying in fees, there are often opportunities to improve. Our role is to provide the clarity and organization you need to make informed decisions about your financial life. That way you can stay focused on what matters most.

The road to financial peace of mind isn’t just about the numbers. It’s about reducing complexity, minimizing fees, and making sure your investments align with your long-term goals. That’s where we come in: helping you streamline your financial life so you can enjoy the journey, not just the destination.